Per chi ne ha voglia, ecco un enorme pippone di McKinsey (prevedo macumbe di Harmattan al solo leggere questo temibile nome

) sulla competitività cinese e sulle sfide poste. Da alcuni punti di vista, le stesse considerazioni si possono applicare al nostro settore manifatturiero rispetto alla competizione di qualità (Germania, Giappone, in alcuni casi USA).

http://www.mckinsey.com/insights/manufacturing/a_new_era_for_manufacturing_in_china?cid=china-eml-alt-mip-mck-oth-1306Intro:

"China’s emergence as a manufacturing powerhouse has been astonishing. In seventh place, trailing Italy, as recently as 1980, China not only overtook the United States in 2011 to become the world’s largest producer of manufactured goods but also used its huge manufacturing engine to boost living standards by doubling the country’s GDP per capita over the last decade. That achievement took the industrializing United Kingdom 150 years.

Today, however, China faces new challenges as economic growth slows, wages and other factor costs rise, value chains become more complex, and consumers grow more sophisticated and demanding. Moreover, these pressures are rising against the backdrop of a more fundamental macroeconomic reality: the almost inevitable decline in the relative role of manufacturing in China as it gets richer.1 Manufacturing growth is slowing more quickly than aggregate economic growth, for example, and evidence suggests that the country is already losing some new factory investments to lower-cost locations, such as Vietnam, sparking concern about China’s manufacturing competitiveness.2

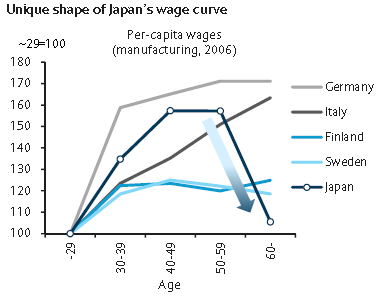

Competitiveness, of course, is a broad term that can confuse more than clarify. During the 1980s, for example, there was much hand-wringing in the United States about declining manufacturing competitiveness versus Japan. In the following decade, however, those concerns faded, replaced by a focus on the failings of “Japan Inc.,” the SUV-fueled resurgence of the US automotive sector, and the boom in US high-tech manufacturing. In the United States then, as in China today, there isn’t just one manufacturing sector; there are many, each with different competitive strengths and weaknesses.

In this article, we move beyond the hyped hopes and frantic fears for Chinese manufacturing as a whole, to gain a more balanced picture of this diverse sector. We start with a summary of four key challenges that affect different types of manufacturers in different ways and then move on to a discussion of competitive priorities whose importance again varies for players of different stripes. Despite the variation across manufacturing subsectors, companies—Chinese owned and multinational alike—can’t escape the need to raise their game and move up the value chain by boosting productivity, refining product-development approaches, and taming supply-chain complexity. Those that do should prosper in the years ahead, while those that rely on yesterday’s model of rock-bottom wages and stratospheric domestic growth rates are likely to fade.

Four challenges

For years, China’s low salaries; strong supply base; high investment in port, road, and rail infrastructure; and solid engineering and technical skills provided a strong platform for manufacturing exports. Meanwhile, a vast domestic market helped fuel China’s continuing transition to a consumption-based economy. Today’s outlook is more mixed. Here, we review four core challenges and the types of players particularly affected by each of them. In doing so, we draw on a set of global manufacturing archetypes established recently by the McKinsey Global Institute.

Rising factor costs

Rising wages and the appreciation of the renminbi have dampened China’s exports in recent years and focused global attention on its future viability as a low-cost manufacturing center. Most multinationals that produce labor-intensive goods, like textiles and apparel, are actively seeking to diversify beyond China to reduce costs and mitigate political and supply-chain risks. China-based processors of goods such as beverages, fabricated metals, food, and tobacco are also concerned about rising costs, including those for packaging. Yet their regional focus makes this less a global competitive issue and more a question of which players in the value chain will create the most value.

Rising consumer sophistication

McKinsey research suggests that by 2020, the income of more than half of China’s urban households, calculated on a purchasing- power-parity basis, will catapult them into the upper middle class— a category that barely existed in China in 2000 (for more, see “Mapping China’s middle class”). The members of this group already demand innovative products that require engineering and manufacturing capabilities many local producers do not yet adequately possess. An executive of a Chinese television-panel maker, for example, recently confessed that his company cannot fully meet the requirements of high-end customers and that the quality of his company’s flat-screen panels is exceeded by that of products from fast-moving South Korean competitors. China’s automakers face a similar challenge: consumers perceive their brands as lower in quality, even compared with foreign brands assembled in nearby Chinese factories.

These issues confront players in a range of other sectors—from appliances and chemicals to electrical and office machinery, pharmaceuticals, telecommunications gear, and transportation equipment. What they have in common is that they compete on the strength of their R&D, technology, and ability to bring customers a steady stream of new products and services. Rising consumer expectations will require even food and beverage players to raise their game on freshness and regulatory compliance, areas where China’s standards still lag behind Western ones.

Rising value-chain complexity

Another big challenge is coping with the rising value-chain complexity that accompanies consumer growth. Greater affluence and rapid urbanization require product makers to manage, make, and deliver an array of increasingly diverse and customized products to increasingly remote locations. Between now and 2015, for example, almost two-thirds of the growth in demand for fast-moving consumer goods will come from smaller (Tier-three and Tier-four) cities, which outnumber their Tier-one counterparts, such as Beijing or Shanghai, by a factor of 20.

Product proliferation and booming e-commerce also contribute to value-chain complexity. Business-to-consumer online sales in China are expected to grow by 45 percent a year from 2010 to 2015. For product makers, this means smaller and smaller lot sizes and deliveries to households farther and farther “out there.” During Chinese festival periods, the supply chains of many companies already creak under the strain of online orders. Demanding consumers contribute to supply-chain headaches, as well. Since many retailers in China accept cash-on-delivery payments, it’s not uncommon for shoppers to pit online retailers against one another by ordering, say, three identical products from three retailers—and refusing delivery to all but the first to arrive.

Such issues are relevant for technology companies and others responding to the Chinese consumer’s increasingly sophisticated tastes. But rising value-chain complexity is also a worry for manufacturers of more labor-intensive goods, given the sheer variety of products they make, and for regional processors, whose logistics networks are affected by urbanization and booming infrastructure development.

Heightened volatility

The uncertain global economic environment since 2008 has complicated life for manufacturers everywhere. Those in China have arguably been the most severely affected, given the country’s status as the workshop of the world.

In China’s steel industry, for example, annual demand growth slowed to 3 percent in 2012, after a decade of double-digit increases. The result has been lower capacity utilization, cutthroat competition, and a 56 percent decline in average profit margins for the industry from 2010 to 2012. Similarly, in China’s massive auto industry, annual growth rates over the past five years have varied from 7 percent to 52 percent.4 Appliance and electrical-machinery producers have also experienced strong demand fluctuations, exacerbated by gyrating overseas demand.

Volatility at such levels makes planning difficult for China’s manufacturers. This is problematic for companies that routinely make large, long-lived capital expenditures whose returns are crucial determinants of performance."

{kind=link}